CPA Exam Sections | Format, Structure, & Content | Each Part Explained

In 2024, the CPA exam saw big changes with the CPA Evolution. The current CPA exam sections are split into two parts: Core and Discipline. The Core sections include:

Let’s look at how the CPA exam is formatted, structured, and scored.

- 1.Becker CPA Review Course: Rated the #1 Best CPA Review Course of 2026

- 2.Surgent CPA Prep Course: Best Technology

- 3.Gleim CPA Review Course: Largest Question Bank

Key Takeaways

- Core and Discipline Structure: The CPA Exam is now divided into Core sections (AUD, FAR, REG) and Discipline sections (BAR, ISC, TCP), allowing candidates to focus on areas relevant to their career goals.

- Content and Skill Assessment: Each section of the exam covers specific content areas and skills, ranging from financial statement audits and compliance to data and technology concepts and applied research.

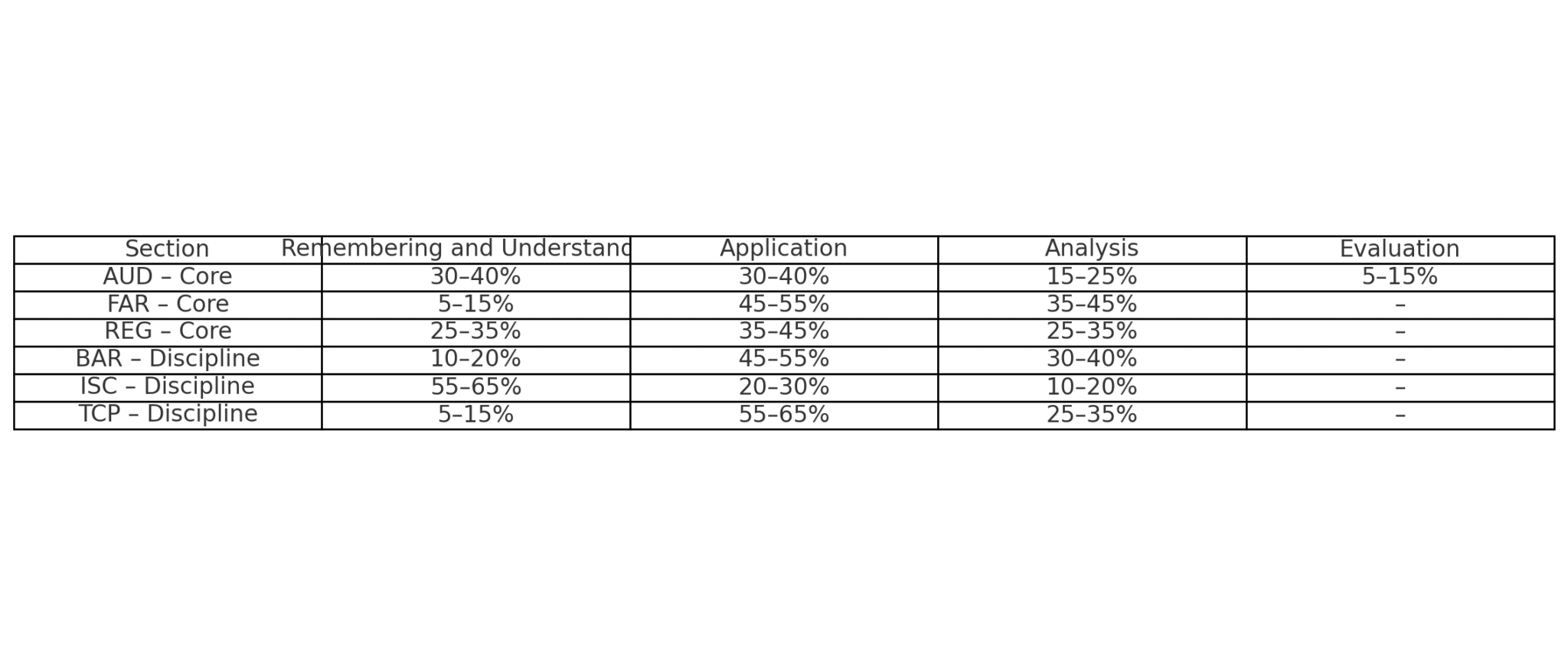

- Question Format: The exam includes multiple-choice questions (MCQs) and task-based simulations (TBSs), with varying difficulty levels that impact scoring. TBS questions are now equally weighted with MCQs, except for ISC, where they count for 40%.

- Exam Preparation: Investing in a CPA review course can significantly enhance your preparation, offering practice questions and simulations that mirror the actual exam format.

CPA Exam Sections’ Content

Each of the Core CPA exam sections encompasses different broad topics that are broken down as follows:

Auditing (AUD)

The AUD section of the CPA Exam evaluates a CPA’s ability to conduct various audit and attestation engagements. These include financial statement audits, compliance audits, internal control audits, and audits of entities receiving federal funds or under ERISA. It also covers assertion-based examinations, direct examinations, and agreed-upon procedures. The assessment focuses on planning, risk assessment, evidence gathering, and reporting, integrating data and technology concepts, professional skepticism, and applied research.

Content is organized into areas, groups, and topics, each with representative tasks that CPAs might perform during engagements. These tasks are examples, not exhaustive lists, and include using auditing standards, verifying data accuracy, and making informed decisions based on evidence.

Content Allocation

- 15–25% – Ethics, Professional Responsibilities and General Principles

- 25–35% – Assessing Risk and Developing a Planned Response

- 30–40% – Performing Further Procedures and Obtaining Evidence

- 10–20% – Forming Conclusions and Reporting

Financial Accounting and Reporting (FAR)

FAR section of the CPA Exam evaluates a CPA’s knowledge and skills in financial accounting and reporting for both for-profit and not-for-profit entities.

The exam covers standards and regulations from:

- Financial Accounting Standards Board (FASB)

- U.S. Securities and Exchange Commission (SEC)

- American Institute of Certified Public Accountants (AICPA)

Key Focus Areas

- Preparation and Review of Financial Statements: Ensuring compliance with applicable frameworks.

- Data and Technology Concepts: Verifying data accuracy and preparing supporting schedules for account balances.

- Applied Research: Using resources like the FASB Accounting Standards Codification to identify issues and determine responses.

- Government Accounting: Foundational concepts related to state and local government accounting from the Governmental Accounting Standards Board (GASB).

Content Allocation

- 30–40% – Financial Reporting

- 30–40% – Select Balance Sheet Accounts

- 25–35% – Select Transactions

Taxation and Regulation (REG)

REG is the only exam that doesn’t explicitly cover accounting topics. It tests a CPA’s knowledge and skills in several key areas:

Key Areas

- U.S. Ethics and Professional Responsibilities: Focus on tax practice.

- U.S. Business Law

- U.S. Federal Tax Compliance: Concentrating on recurring and routine transactions for individuals and entities.

Federal Tax Compliance

- Preparation and Review of Tax Returns: Evaluates a CPA’s role in preparing and reviewing tax returns.

- Data and Technology Concepts: Verifying the completeness and accuracy of data used in tax returns, and utilizing automated validation checks and diagnostic tools to identify potential errors.

- Applied Research: Using resources like the Internal Revenue Code and Treasury Regulations to identify issues, analyze facts, and determine appropriate responses.

Content Allocation

- 10–20% – Ethics, Professional Responsibilities and Federal Tax Procedures

- 15–25% – Business Law

- 5–15% – Federal Taxation of Property Transactions

- 22–32% – Federal Taxation of Individuals

- 23–33% – Federal Taxation of Entities (including tax preparation

Check out the best REG study tips!

Business Analysis and Reporting (BAR)

If you’re a CPA candidate eyeing roles in assurance or advisory services, financial statement analysis, or financial and operations management, the BAR discipline might be your best bet. This area covers:

- Data analytics

- Financial risk management

- Financial planning techniques

You’ll also explore advanced topics such as revenue recognition, leases, business combinations, derivatives, hedge accounting, and employee benefit plan financial statements.

Content Allocation

- 40–50% – Business Analysis

- 35–45% – Technical Accounting and Reporting

- 10–20% – State and Local Governments

Information Systems and Controls (ISC)

For those interested in technology and business controls, the ISC discipline is a great fit. It’s geared toward CPA candidates focusing on:

- Business processes

- Information systems

- Information security and governance

- IT audits

Key areas include IT and data governance, internal control testing, and information system security, such as network security, software access, and endpoint security.

Content Allocation

- 35–45% – Information Systems and Data Management

- 35–45% – Security, Confidentiality, and Privacy

- 15–25% – Considerations for System and Organization Controls (SOC) Engagements

Tax Compliance and Planning (TCP)

If taxation piques your interest, the TCP discipline is tailored for you. This focuses on advanced individual and entity tax compliance, including:

- Personal financial planning

- Entity planning

- Inclusions and exclusions to gross income

- Gift taxation compliance and planning

Advanced topics may cover consolidated tax returns, multijurisdictional tax issues, and transactions between entities and their owners. You’ll also explore the tax treatments of forming and liquidating business entities.

Content Allocation

- 30–40% – Tax Compliance and Planning for Individuals and Personal Financial Planning

- 30–40% – Entity Tax Compliance

- 10–20% – Entity Tax Planning

- 10–20% – Property Transactions (disposition of assets)

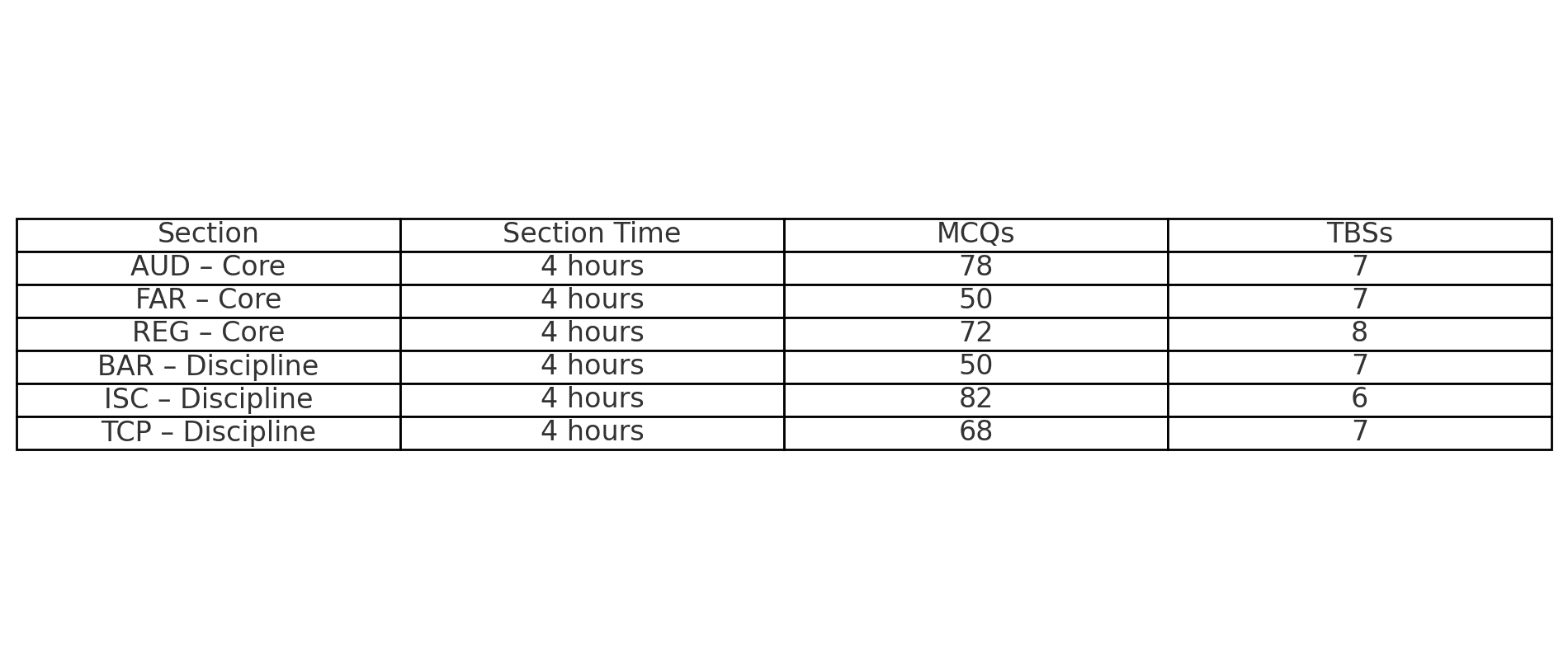

CPA Exam Sections Structure and Format

Each exam part is formatted into question blocks called testlets. These testlets contain either multiple-choice questions or task-based simulations. Additionally, each test starts out with several MCQ testlets followed by several Task-Based Simulation (TBS) testlets.

Multiple-Choice Question Testlets

Multiple-choice questions vary in difficulty and change as you correctly or incorrectly answer questions. For instance, each exam section starts with a medium-difficulty MCQ testlet. Consequently, if you perform well on this testlet, you will receive a more difficult MCQ testlet on your second one. If you do well on this difficult testlet, you will receive an even more difficult group of questions on your third one. However, the opposite is true if you perform poorly on any testlet. Here’s what it looks like:

You might think, “Oh, this is good. I can make my exam easier by performing poorly on the first set of questions.” Wrong. You actually want more difficult questions because they are weighted more. Basically, one correctly answered difficult question will do more for your overall score than multiple correctly answered easy questions. Therefore, you are way better off answering difficult questions.

Hidden amongst the operational questions are pretest questions. These are questions that the AICPA is currently testing to see if they should include them on future exams. They are indistinguishable from normal testing questions, and the answers will not affect your overall score.

Task-Based Simulation Testlets

Task-based simulations are problem set that allows you to apply your knowledge and demonstrate that you understand the topics on the exam. They are formatted differently on each exam part, but the most common formats include matching and fill-in-the-blank. Each part also includes one research question that requires you to research a topic in the authoritative literature and cite the code that discusses the current topic at hand. Most candidates feel these are more difficult than MCQs.

No two exams have the same number of questions and simulations, but you will have to navigate through each exam in a four-hour period. Currently, TBS questions equate to around 50% of your exam score for most tests.

Worried about doing well on simulations?

Investing in a CPA review course is usually the answer since they have exam-like questions for you to practice with.

Get Discounts On CPA Review Courses!

Save $1,800 on UWorld CPA Elite-Unlimited+ Course

Flash Sale – $1,600 Off UWorld CPA Elite-Unlimited Course

Take $1,500 Off UWorld CPA Premier Course

Save $1,350 on Becker CPA Concierge

Take $1,346 Off Becker CPA Pro+

Enjoy $1,346 Off Becker CPA Pro

Save $1,250 on Gleim CPA Traditional

Enjoy $1,225 Off Gleim CPA Premium Pro Course

Take $750 Off Gleim CPA Premium

Take $510 Off Surgent CPA Ultimate Pass

Get CPA Evolution Ready Content on All Becker CPA Courses – Deal

Becker CPA: Interest-Free Payment Plan – Deal

Becker CPA Advantage Package Now $2,499 – Promo

Enjoy a 14-day Free Trial on Becker CPA Courses

Exclusive Student Discount: Up to 46% Off Gleim CPA Review

Becker Deal: Save on CPA Single Part Courses

Exclusive Offer – 30% Off Lambers CPA Course Package

Enjoy 7-Day Free Trial on UWorld CPA

Save $629 Surgent CPA Ultimate Pass

CPA Exam Scoring

The AICPA keeps changing the way it grades and weights the multiple-choice questions on the exam. It wasn’t that long ago that the questions were worth more than 70 percent of the total points on the test. That’s crazy. Each question was worth a ton.

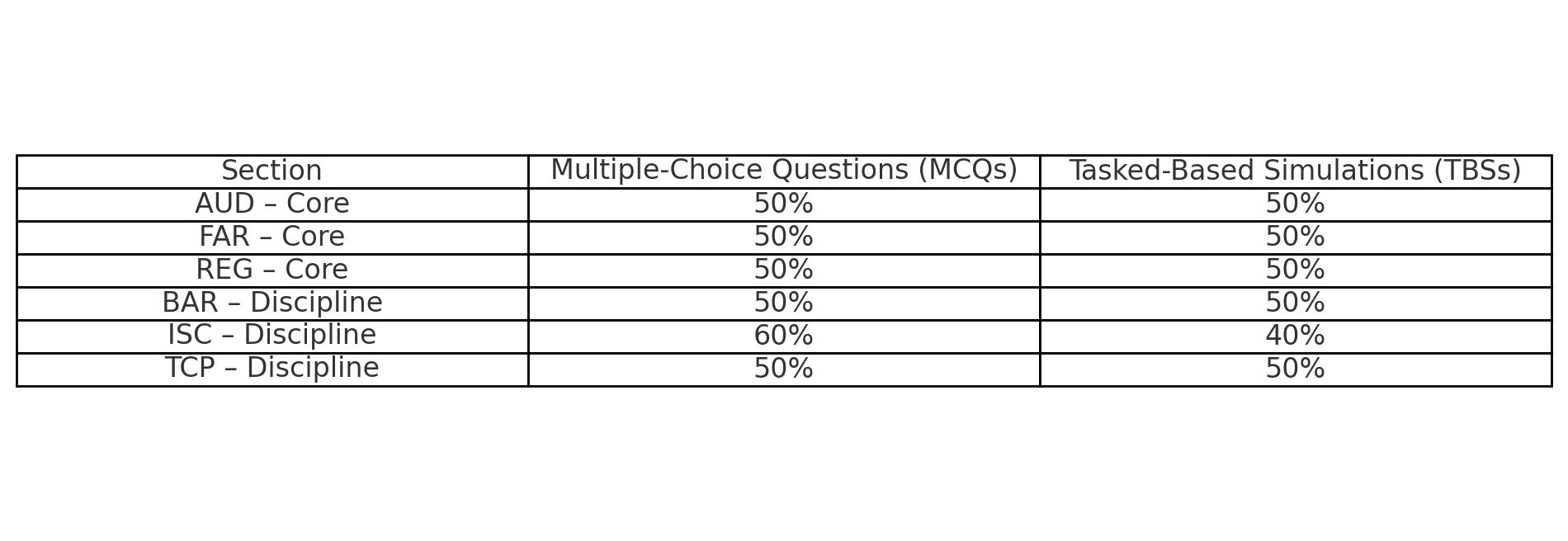

In recent years, they have been backing off the value of MCQs and putting more importance on task-based simulations. The MCQs are weighted evenly with the simulations. Thus, the MCQs are only worth 50 percent of your points and the simulations are worth the other 50 percent. The only exception for this is the ISC Discipline, in which TBS only counts for 40%

Here’s a breakdown of how the CPA exam is graded and weighted.

Conclusion

In 2024, the CPA exam underwent significant changes with the introduction of the CPA Evolution. The exam now consists of Core and Discipline sections, providing candidates with a more focused and specialized approach to testing. Understanding these changes and the structure of the exam is crucial for effective preparation and success.

FAQ

What are the major changes in the CPA Exam as of 2024?

In 2024, the CPA Exam was restructured into Core and Discipline sections. The Core sections are Auditing & Attestation (AUD), Financial Accounting & Reporting (FAR), and Taxation and Regulation (REG). Candidates now choose from Business Analysis & Reporting (BAR), Information Systems and Controls (ISC), or Tax Compliance and Planning (TCP).

How is the CPA Exam structured and what types of questions are included?

Each section of the CPA Exam lasts four hours and includes multiple-choice questions (MCQs) and task-based simulations (TBSs). MCQs adjust in difficulty based on performance, with harder questions carrying more weight. TBSs test practical knowledge application and are equally weighted with MCQs, except in ISC, where TBSs account for 40% of the score.

What topics are covered in the Core sections of the CPA Exam?

The AUD section focuses on audit and attestation engagements. FAR covers financial accounting and reporting standards for both for-profit and not-for-profit entities. REG assesses knowledge in U.S. ethics, business law, and federal tax compliance for individuals and entities.

What are the specialized topics covered in the Discipline sections of the CPA Exam?

BAR includes data analytics, financial risk management, and advanced accounting topics. ISC focuses on business processes, information systems, and IT audits. TCP covers advanced tax compliance for individuals and entities, personal financial planning, and entity tax planning.

How should I prepare for the task-based simulations on the CPA Exam?

Task-based simulations test the practical application of knowledge through matching, fill-in-the-blank questions, and research tasks. Investing in a CPA review course that offers practice simulations can help familiarize you with the exam format and improve your ability to apply concepts in real-world scenarios.

Kenneth W. Boyd is a former Certified Public Accountant (CPA) and the author of several of the popular "For Dummies" books published by John Wiley & Sons including 'CPA Exam for Dummies' and 'Cost Accounting for Dummies'.

Ken has gained a wealth of business experience through his previous employment as a CPA, Auditor, Tax Preparer and College Professor. Today, Ken continues to use those finely tuned skills to educate students as a professional writer and teacher.

Learn More

What Are the Requirements to Take the CPA Exam?

CPA exam requirements are set by individual state boards and thus vary by state jurisdiction. Although every state board of accountancy has slightly different requirements to sit for the CPA examination, most states have the same core set of qualifications that candidates must meet in order to be eligible. Let’s take a look at what…

CPA Exam Schedule [2026 Dates, Testing Windows, & Blackout Months]

The CPA exam schedule is pretty confusing because there are so many different testing windows, exam dates, blackout months, and other oddities. This means that the scheduling process can be difficult to figure out for first-time candidates. But it doesn’t have to be. Here is some “must-know” info about the CPA exam scheduling, with tips…

Which Section of the CPA Exam Should You Take First?

When you have to take four notoriously difficult exams in a row? It’s important to know which to take first. You want to start off on the right foot: build confidence, momentum, and excitement for the rest of your journey. But the right “first section” isn’t the right choice for every candidate. In this guide,…

Best CPA Exam Review Self-Study Books of 2026

There are many different CPA exam review books on the market today. Some are better than others and some are just different. Therefore, how are you supposed to know which ones are right for you? First, you need to look at your learning style to understand what type of CPA study book you should be…

What is the Best Order to Take the CPA Exam Sections?

There are several different theories on the best order to take the CPA exam sections. Because with pass rates as low as 41%, it’s worth doing everything you can to boost your odds, including perfecting your order strategy. Today, I want to share mine. It’s a little bit different, but it worked for me. I’m…

Which CPA Exam Section is the Hardest?

Historically, there were four CPA exam sections. Now, CPA candidates have three “core” sections they have to take, and three discipline sections they have to choose a single section from. All of that is to say: to some extent, you can choose how hard your exam path is going to be. For the three exams…